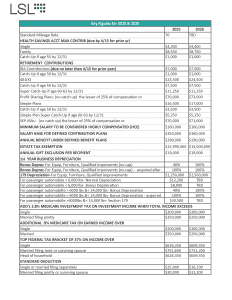

It’s commonly known that Federal and California tax law prohibits California from taxing a nonresident’s income from retirement plan distributions, even though contributions to these plans were made while living in California. What many aren’t aware of is that this rule can also apply to certain payments from nonqualified deferred compensation plans or, for retiring partners, any written plan, program, or arrangement that provides for retirement payments in recognition of prior service.

For these payments to qualify, they’re required to be made for either:

- The life or life expectancy of the recipient (or the joint lives or joint life expectancy of the recipient and the designated beneficiary of the recipient); or

- A period of not less than ten years

Discuss Payment Plans Before You Leave California

As many California residents look at retiring out of state—if they have nonqualified plans—they should be reviewing how these payments will be paid. Discussing how the payments from the nonqualified plans and/or from a partnership they may be leaving should be paid out can help to avoid this income being subject to California taxation. Starting these discussions early will allow time to see if there are options to negotiate the terms of the payments.

For example, in structuring payments, assume Bill has worked for a consulting firm in Los Angeles for 20 years. As part of his retirement package, he will receive $1 million in nonqualified deferred compensation. Bill has the option of receiving those payments over a five-year or ten-year term.

Choose a Ten-Year or Five-Year Term Ahead of Time

Bill is going to retire in Texas. If he chooses the ten-year term, all payments he receives after he moves to Texas will not be subject to California tax since the period of the payments is not less than ten years. In addition, since Texas doesn’t have personal income tax, his payments would be tax-free for state tax purposes.

On the other hand, if Bill chooses the five-year term, all of the payments would be subject to California since the period of the payments is less than ten years.

An additional thing to keep in mind is that California looks to a nonresident’s worldwide income for purposes of determining the tax rate to apply. If Bill’s total annual income is more than $406,000, he would pay California tax of 11.3% on those deferred compensation payments.

Conclusion

Federal and California tax laws prohibit California from taxing a nonresident’s income from retirement plan distributions. It appears that these laws can also apply to certain payments from nonqualified deferred compensation plans over certain time frames. In general, spreading the payments for more than ten years will avoid California taxes, depending on one’s total annual worldwide income.

Bottom line: For retirees moving out of state, the best course is to start planning early. They should check for options to negotiate payment terms—the goal being to legally avoid California income tax and have more money to live on in retirement.

So, it’s wise to think ahead, and it’s best to ask a qualified CPA for their advice. LSL CPAs can help.