Many taxpayers focus on finding deductions at tax time. The challenge is that by the time tax season arrives, most of the decisions that impact your tax liability have already been made.

One of the most powerful concepts in tax planning is simple: If you want to change your tax, you have to change your facts.

In other words, meaningful tax savings often come from changing how income is earned, how investments are structured, and what activities you’re participating in throughout the year—not from searching for last-minute deductions in April.

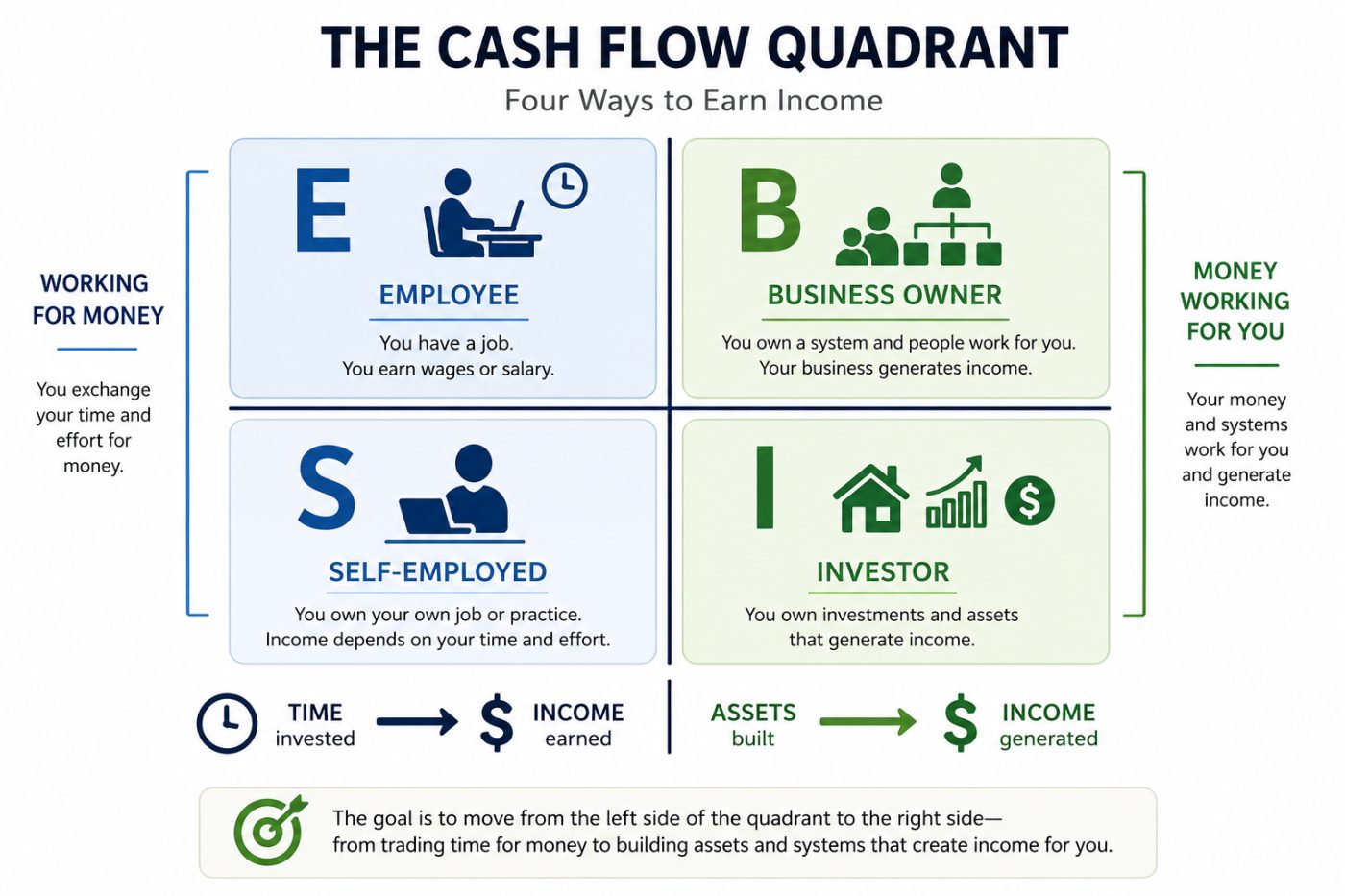

A helpful framework for understanding this concept comes from Robert Kiyosaki’s Cash Flow Quadrant, which illustrates how different types of income are taxed and why proactive planning matters.

Understanding the Cash Flow Quadrant

The Cash Flow Quadrant divides income into four categories:

E – Employee

Employees earn wages and salaries from an employer. Their income is generally reported on a W-2, and tax planning opportunities can be more limited because many expenses are not deductible at the individual level.

S – Self-Employed

Self-employed individuals own their jobs rather than owning a system that operates without them. Consultants, independent contractors, and many small business owners fall into this category.

While self-employed individuals often have more tax planning opportunities than employees, they may also be subject to self-employment taxes in addition to income taxes.

B – Business Owner

Business owners build systems, teams, and organizations that can generate income beyond their direct labor.

This distinction matters because the tax code includes numerous provisions designed to encourage business investment, job creation, and economic growth. As a result, business owners often have access to planning opportunities that may not be available to employees.

I – Investor

Investors generate income through investments such as real estate, businesses, and other assets.

Different types of investment income may receive different tax treatment than earned income, creating additional planning opportunities when structured appropriately.

Why the Source of Income Matters

One of the key lessons of the Cash Flow Quadrant is that where your income comes from can be just as important as how much income you earn.

The tax code contains thousands of pages of rules, deductions, credits, incentives, and special provisions. Many of these provisions were created to encourage specific economic activities such as:

- Business investment

- Housing development

- Energy production

- Agricultural activities

- Technological innovation

Understanding these incentives can help taxpayers make more informed decisions about their financial strategies.

The Difference Between Working for Money and Having Money Work for You

Another important distinction within the Cash Flow Quadrant is the difference between active and passive income.

Individuals on the left side of the quadrant (Employees and Self-Employed) generally earn income by trading time and expertise for compensation. If they stop working, income often slows or stops as well.

Individuals on the right side of the quadrant (Business Owners and Investors) are often focused on building assets, systems, and investments that can generate income independently of their day-to-day involvement.

While every situation is different, many long-term wealth-building strategies involve gradually increasing participation in business ownership and investment activities.

A Simple Framework: Turn Up the HEAT

When discussing proactive tax planning, one useful way to think about opportunities is through the acronym HEAT:

H – Housing

Real estate and housing-related investments can provide a variety of tax benefits depending on the structure, use, and ownership of the property.

Potential opportunities may include depreciation, cost segregation studies, and other real estate-related planning strategies.

E – Energy

Federal and state governments have historically offered incentives designed to encourage investment in energy-related projects.

Depending on the circumstances, taxpayers may benefit from various credits, deductions, and incentives associated with qualifying energy investments.

A – Agriculture

Agricultural activities can provide unique planning opportunities and may qualify for certain tax benefits that are unavailable in other industries.

For some taxpayers, agricultural investments may become part of a broader diversification and tax planning strategy.

T – Technology

Innovation is heavily encouraged throughout the tax code.

Businesses that invest in research, development, process improvements, software development, or technological advancement may qualify for incentives such as research and development (R&D) tax credits and other tax-saving opportunities.

The Importance of Strategic Tax Planning

Perhaps the biggest takeaway is this:

Tax planning should happen throughout the year, not just during tax season.

Many taxpayers meet with a tax preparer once a year to file returns and report what already happened. While tax preparation is important, it is fundamentally a historical exercise.

Tax strategy is different.

A tax strategist works proactively to identify opportunities before the year ends, helping taxpayers evaluate potential decisions, investments, business activities, and transactions that could impact future tax outcomes.

The earlier these conversations occur, the more options are typically available.

Questions to Ask Yourself

As you think about your own tax situation, consider:

- Where does most of my income come from today?

- Am I primarily earning income as an employee, self-employed individual, business owner, or investor?

- Are there opportunities to diversify how I earn income?

- Have I explored tax incentives related to housing, energy, agriculture, or technology?

- Have I met with a tax strategist this year to discuss proactive planning opportunities?

Final Thoughts

Reducing taxes is rarely about finding a secret deduction or a last-minute loophole. More often, it’s about making intentional decisions throughout the year that align with both your financial goals and the incentives built into the tax code.

The most effective tax plans begin long before a tax return is prepared. They start with understanding your current situation, evaluating your options, and making strategic decisions that can help create better outcomes over time.

Because when it comes to tax planning, changing your tax often starts with changing your facts.

If you want to start changing your facts – contact us today!